Lifenet Life Insurance Co., Ltd.

Lifenet Life Insurance Announcement of the release of new medical insurance – Scheduled to release “Jibun no Hoken Z (Z)”, a term-type medical insurance with a choice of insurance period from 10 years, in October

……

Lifenet Life Insurance Co., Ltd. (URL:

https://www.lifenet-seimei.co.jp/

Since its establishment, Lifenet Life has been based on the premise that Japan is a society with ample public security as exemplified by the public medical insurance system, and has been providing medical insurance specializing in necessary coverage such as hospitalization and surgery. We have been offering the “Insurance for Yourself” series. In order to realize a “society where future generations can be raised with peace of mind,” we have launched a “term-type” medical insurance that allows you to choose between 10, 20, and 30 years, with the aim of being an insurance that will continue to be chosen by the younger generation. We will develop and strengthen the lineup of the “Insurance for myself” series.

Particularly among the younger generation, whose life plans are changing, medical insurance is also becoming more and more common. With the advent of NISA and iDeCo, it has become easier to build assets through methods other than life insurance, so Lifenet Life once again proposes that the origin of insurance is “security.” Especially for the younger generation, considering that life plans tend to fluctuate and incomes are difficult to stabilize, securing insurance through a term-type insurance policy with low premiums is a reasonable option. Sho.

Term insurance tends to be seen as a disadvantage because premiums increase when it comes to renewal, but if you have sufficient savings, are on track to build assets, or have finished raising children, you may turn to insurance. You can adjust your insurance premium burden by canceling your policy when you no longer need it or reducing your coverage. In fact, Lifenet Life insurance policyholders have put into practice two ways of using their insurance: “Cancel the policy because your child is entering the workforce,” and “Cancel the policy because your child is now able to prepare for emergencies on his own.”* 1.

In other words, insurance is something that is regularly reviewed in line with changes in life and the need for protection, and just as the landscape of a family changes dramatically after 10 years, it is important to update the way you have insurance every 10 years. It’s important.

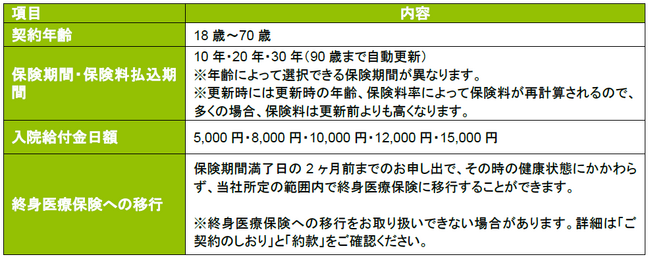

Term medical insurance “Jibun no Hoken Z” and “Jibun no Hoken Z Ladies” not only allow you to set the insurance period in 10-year increments, but also inherit the features of whole life medical insurance “Jibun no Hoken 3”. I’m here. You can choose from two options: the Economy course for those who are generous with short-term hospital stays and value low insurance premiums, and the recommended course for those who want coverage for cancer and advanced medical care. Term medical insurance that can save you money.

Features of term medical insurance “Jibun no Hoken Z” and “Jibun no Hoken Z Ladies”

(Please see “Reference Materials” for product overview)

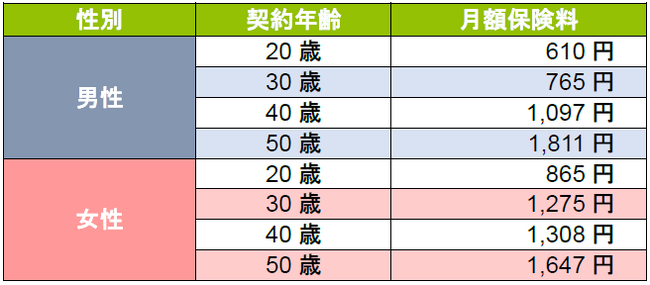

[Table 2: Monthly premium

Typical monthly premiums for the term medical insurance “Jibun no Hoken Z” are as follows.

Coverage details: Economy course, hospitalization benefit 5,000 yen per day/insurance period/premium payment period 10 years

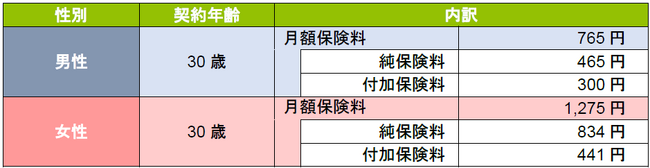

Of the insurance premiums paid by customers, our company discloses the additional insurance premiums, which are expenses related to the life insurance company’s personnel costs and stores. As an example, the breakdown of net insurance premiums and additional insurance premiums for a contract age of 30 years is as follows.

Coverage details: Economy course, hospitalization benefit 5,000 yen per day/insurance period/premium payment period 10 years

The breakdown of insurance premiums (representative examples) for other insurance products can be viewed on our website.

https://www.lifenet-seimei.co.jp/about/

Japanese people have too much insurance, a state of “insurance dependence” Lifenet Life is based on the “Lifenet Life Insurance Manifesto” and has three important points when developing insurance products.

In this way, the reason why Lifenet Life places emphasis on not providing excessive coverage and keeping life insurance premiums low is because Japanese people have ample public security, as represented by the public medical insurance system. This is because even though we live in a society where many people live in such a society, we are still dependent on insurance.

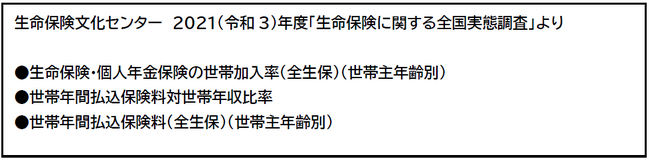

The household participation rate for life insurance*2 is 89.8% overall, and over 90% for those aged 30 to 34. Moreover, the average annual premium paid by households is 371,000 yen as a whole, and even for those aged 30 to 34, the average is 262,000 yen, meaning that even people in their early 30s pay approximately 21,833 yen per month as insurance premiums. The burden of insurance premiums accounts for 6.7% of annual household income, which is not a small burden. If you think about it in terms of take-home income, you can imagine that it’s an even bigger expense.

*All life insurance includes private insurance (including Japan Post Insurance), Kampo, JA, prefectural mutual aid, co-op, etc. For those over 90 years old, the sample is less than 30

I buy life insurance through someone else because I don’t think I know anything about insurance.

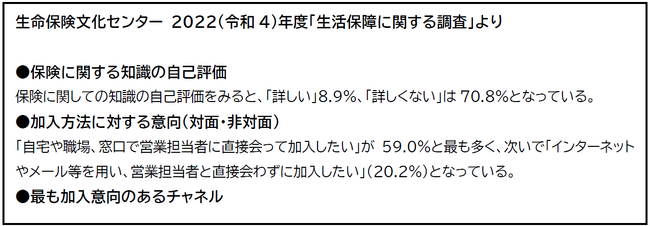

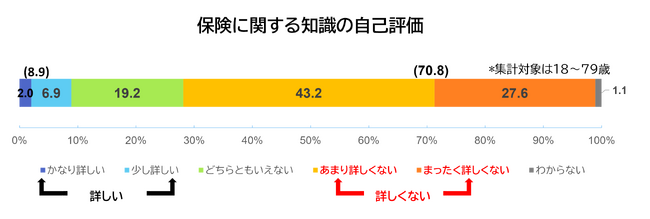

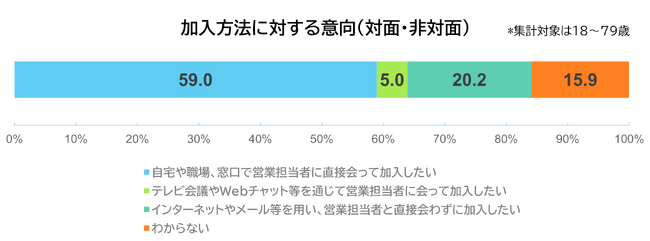

On the other hand, when asked about their self-assessment of knowledge about insurance, 70.8% of people answered that they were not familiar with it.*3 79.1% of men in their 20s, 85.2% of women, 69.8% of men in their 30s, and 77.9% of women answered that they did not know much about insurance. This shows that many people subscribe to life insurance, despite the perception that they don’t know much about it. In addition, regarding “intentions regarding enrollment method (face-to-face/non-face-to-face),” 59% of respondents prefer “face-to-face,” indicating that mail-order sales, which require you to select insurance products and complete the procedures yourself, are the channel for those who intend to enroll. Only 17.7% of people chose it as such.

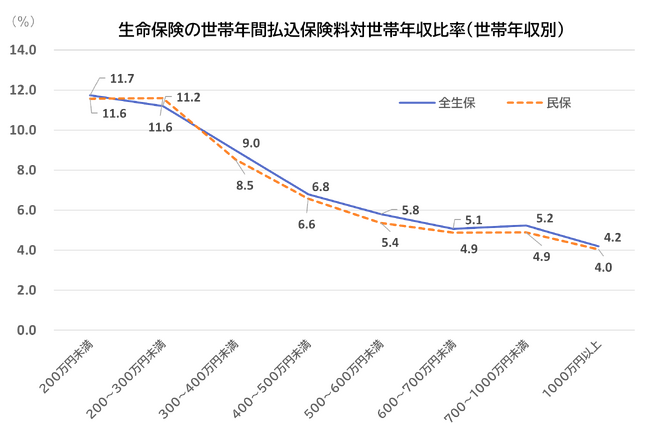

In other words, the current situation in Japan can be summarized as people who do not know anything about insurance, so they buy life insurance through someone else, and pay an average annual premium of 371,000 yen. The impact that insurance premiums have on household finances is greater the lower the annual income.For households with an annual income of less than 3 million yen, the annual insurance premiums paid exceed 11% of the annual income*4, and in addition, they pay social insurance premiums. Therefore, it can be said that it is not an extreme theory that Japanese people are “dependent on insurance” and “have too much insurance.”

*All life insurance includes private insurance (including Japan Post Insurance), Kampo, JA, prefectural mutual aid, consumer cooperatives, etc.

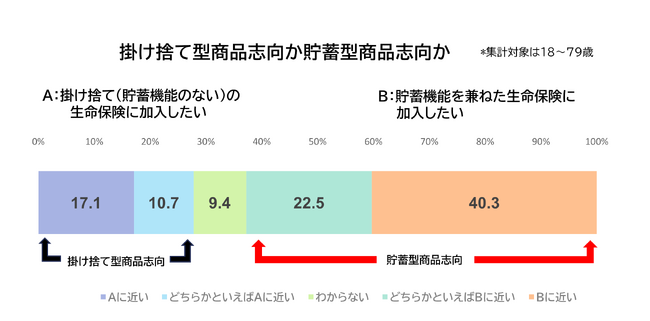

I want to make it commonplace to think about insurance and increasing money separately.

It seems that choosing to take out insurance with a savings function is more preferred than taking out protection-type insurance with lower premiums, which is called a discount insurance *5. 60% of people are “oriented towards saving-type products.” The answer is yes. However, in reality, the “expected interest rate” of life insurance has been low for a long time, and even considering that we are in the so-called “ultra-low interest rate era,” choosing to purchase insurance for the purpose of increasing money is not necessarily the original purpose. It may not be said that it matches.

Since its establishment, Lifenet Life has provided only insurance products that specialize in protection, and we have been offering customers the opportunity to reduce insurance premiums and increase their money by choosing the best financial products available in the world. I have recommended it. I am convinced that what the world needs now is term-type, disposable insurance that can be purchased online, so that it will become more commonplace in the future to rely on insurance for protection and to save and build assets yourself. I am. Although it is a term insurance that specializes in protection, which is not the mainstream among insurance products, it is the ideal form of insurance, and we will continue to develop it so that it will become a new standard as it is easy to use for today’s young generation. We would like to actively disseminate information and spread awareness.

*1 From the Lifenet Life Insurance cancellation survey

*2, *4 From the Life Insurance Culture Center 2021 (Reiwa 3) “National Survey on Life Insurance” (published in December 2021)

*3, *5 From the Life Insurance Culture Center 2022 (Reiwa 4) “Survey on Life Security” (published in March 2023)

Reference materials: Overview of term medical insurance “Jibun no Hoken Z” and “Jibun no Hoken Z Ladies”

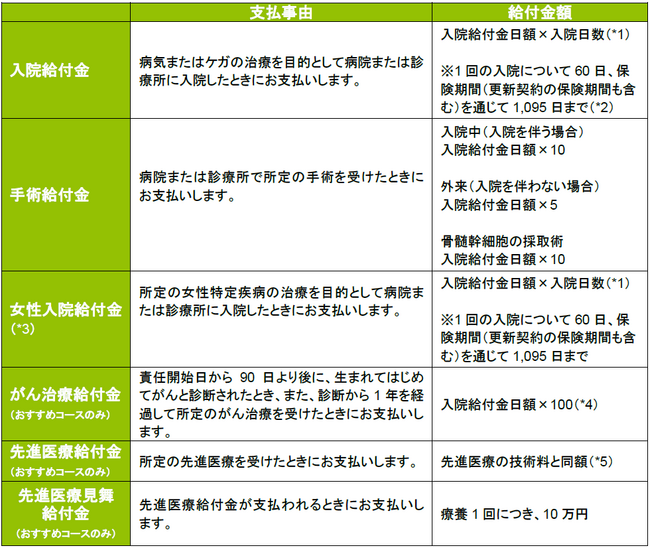

About each benefit

*1 If you are hospitalized for less than 5 days, including day hospitalization, you will be paid 5 days worth of daily

hospitalization benefits.

*2 For the recommended course, if you are hospitalized for the purpose of treatment for one of the three major lifestyle-related diseases, the maximum number of payment days is unlimited.

*3 “Insurance for myself Z Ladies” only

*4 Payments will be made once a year up to a maximum of 5 times throughout the insurance period (including the insurance period for renewal contracts)

*5 Up to 20 million yen throughout the insurance period (including the insurance period of renewal contracts)

*The information listed here is a summary of the warranty details. Details will be posted on the website after sales begin.

About Lifenet Life URL: https://www.lifenet-seimei.co.jp/

Lifenet Life has summarized its management philosophy of “supporting each customer’s lifestyle by operating honestly and providing easy-to-understand, inexpensive, and convenient products and services” in the “Lifenet Life Insurance Manifesto.” Since the start of our operations, we have consistently delivered life insurance from the customer’s perspective. As a leading online life insurance company, we aim to create a society where future generations can be raised with peace of mind by utilizing digital technology.